7 FinTech API Use Cases Revolutionizing Financial Services

Quick Answer: Fintech APIs let product teams connect payment rails, KYC/AML checks, PSD2 open banking data, virtual accounts, market data, crypto infrastructure, and OCR workflows without rebuilding regulated financial plumbing from scratch. For CTOs, the main decision is not “which API is popular,” but which provider fits the architecture, data residency, audit trail, SLA, and compliance model of the product.

The number of fintech API calls is projected to surge nearly 500% from 2023 to 2027. The growth is tied to open banking API adoption, embedded finance, stronger KYC/AML automation, and product teams exposing financial capabilities through REST, webhooks, OAuth 2.0, tokenized account access, and cloud-native event pipelines.

This article maps seven fintech API use cases that matter when building a regulated financial product: payment processing, identity verification, banking integration, virtual accounts, cryptocurrency infrastructure, market data access, and OCR or machine learning document automation. Each use case includes API examples, business fit, and implementation risks that a CTO, product owner, or compliance lead should validate before integration.

What are FinTech APIs?

Fintech APIs are application programming interfaces that let financial software connect with payment processors, banks, KYC providers, market data vendors, blockchain infrastructure, and document automation platforms. In production, fintech APIs usually expose REST or GraphQL endpoints, OAuth-based authorization, webhook notifications, sandbox environments, audit logs, and compliance controls for GDPR, PSD2, AML, and local financial regulations.

What are the benefits of using FinTech APIs?

FinTech APIs reduce implementation risk when the integration is treated as infrastructure, not a plug-in. The strongest business case appears when an API replaces regulated, high-maintenance capabilities such as card acquiring, ACH transfers, PSD2 account information access, identity verification, transaction categorization, or invoice OCR.

- Lower development cost: FinTech APIs provide pre-built financial capabilities, reducing the need to build payment orchestration, bank connectivity, ID document validation, or reconciliation logic from scratch.

- Shorter time to market: A financial data API, payment API, or KYC API can compress discovery-to-MVP timelines when the provider offers a stable sandbox, SDKs, webhook documentation, test credentials, and clear rate limits.

- Compliance support: Mature API providers help with GDPR, PSD2, AML, KYC, PCI DSS, and audit evidence through standardized data handling, encryption, access controls, consent flows, and reporting artifacts.

7 FinTech API use cases transforming financial services

The seven use cases below cover the most common API decisions in fintech product architecture. For each one, validate provider SLAs, regional coverage, data retention, incident response, authentication model, webhook reliability, and how the API behaves under failed payments, expired consents, duplicated events, and partial outages.

Payment processing

Payment processing APIs are the transaction layer for card payments, digital wallets, bank transfers, recurring billing, refunds, chargebacks, and settlement reporting. The API choice affects PCI DSS scope, checkout conversion, reconciliation workload, and how much payment orchestration logic the product team must maintain.

In a production architecture, payment APIs usually combine tokenization, hosted checkout or embedded components, webhook-based event delivery, idempotency keys, fraud scoring, and settlement exports. CTOs should test retry logic, refund paths, chargeback handling, payment method coverage, and integration with accounting or subscription systems before selecting a provider.

Ideal for: E-commerce platforms, subscription services, retail stores, and software developers/startups needing online payment capabilities.

API examples:

- Stripe: Takes care of the entire payment process, from transaction initiation to funds settlement, allowing businesses to accept payments from credit cards, debit cards, and digital wallets.

- Braintree: Allows developers to integrate its global payments platform, supporting various payment methods, including cards, wallets, and local payment methods.

- MangoPay: Facilitates online banking transactions, especially in crowdfunding, marketplace, and sharing economy platforms.

- GoCardless: Enables collecting payments via a single integration, including automated payment collection and reconciliation.

Case study:

DocuSign is a global SaaS brand that helps businesses manage electronic agreements, and is on a mission to accelerate business and simplify life for companies of all sizes.

DocuSign identified a gap in their payment options, especially in countries where debit purchases are so popular like the Netherlands and Germany. GoCardless's API provided a way for Docusign to integrate this new bank payment option to customers directly in their existing subscription management platform, Zuora.

Identity verification (KYC)

Identity verification APIs automate KYC and AML checks for regulated onboarding. They validate names, addresses, dates of birth, government-issued IDs, sanctions lists, politically exposed person data, liveness checks, and biometric signals, depending on jurisdiction and provider configuration.

For a CTO, KYC API selection should include false positive rates, manual review queues, AML screening depth, explainability of verification decisions, data residency, retention policy, and evidence exports for regulators or banking partners. The technical integration should also account for step-up verification, retry flows, expired documents, and webhook events that arrive out of order.

Ideal for: Financial institutions, fintech companies, e-commerce platforms, and any business needing to verify user identities.

Example APIs:

- Trulioo API: Provides global identity verification services to help businesses comply with KYC and AML regulations by verifying customer identities across multiple countries.

- Jumio API: Provides identity verification services using document verification, facial recognition, and authentication technologies to ensure secure and compliant onboarding.

- Onfido API: Offers automated identity verification and background checks by validating government-issued IDs and performing biometric verification to authenticate users.

- IDnow API: Facilitates real-time identity verification through video identification and e-signature capabilities, ensuring compliance with KYC regulations.

- Shufti Pro API: Provides identity verification and KYC services, including document verification, face verification, and AML screening, to help businesses comply with regulatory standards.

Case study:

STACK, a fintech API, combines advanced machine learning with customizable tools to help millennials reach their financial goals with automated savings, weekly budgeting, and fee-free services while also rewarding them in real-time with offers from merchants where they shop.

But STACK needed digital identity verification to quickly, securely and smoothly on board members while maintaining compliance with Anti-Money Laundering (AML) and KYC regulations. STACK leverages Trulioo during member onboarding to verify identities and meet AML, KYC and FINTRAC requirements.

Banking integration

Banking integration APIs connect products to account information, balances, transaction history, payment initiation, and consent management. Open banking APIs changed the default from screen scraping and static bank exports to regulated access patterns based on user consent, secure authentication, and standardized data exchange.

The current phase, often called open finance, extends access patterns beyond current accounts into savings, mortgages, insurance, payroll, and credit products. Engineering teams should validate PSD2 coverage, consent renewal UX, bank uptime variance, data normalization quality, and how the API handles inconsistent merchant names, pending transactions, and multi-currency accounts.

Ideal for: Personal finance apps, budgeting tools, multi-bank management platforms, bookkeeping software, payroll systems, and expense management software.

Example APIs:

- Plaid: Allows developers to securely link bank accounts to other applications, without users having to leave their site.

- Syncfy Connect: Enables financial data retrieval directly from the source using Open Finance; imports data from banks, utility providers, digital wallets, credit cards, and major blockchain networks.

- Yodlee: Combines financial insights with data from 17,000 sources and is designed to make transaction data easier to understand.

- MX: Aggregates and enhances financial data, empowering organizations to provide better financial experiences for their customers.

- Finicity: Offers an open banking platform and data aggregation solution, powered by Mastercard.

Case study:

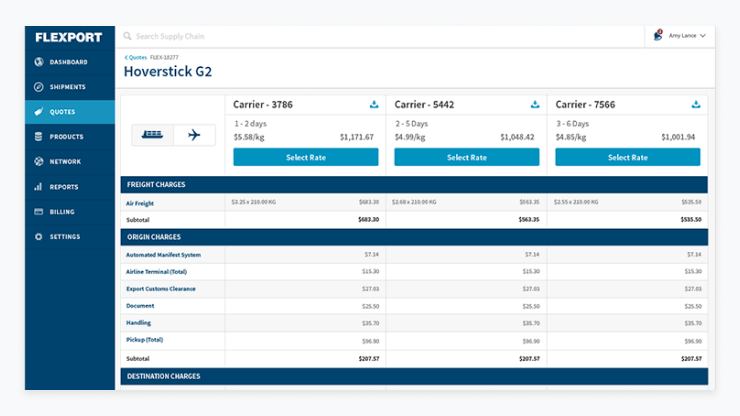

Flexport is a global trade technology company that provides buyers, sellers, and their logistics partners with the technology and freight services needed to grow and innovate. To meet their clients' full financing needs more effectively, Flexport required timely information. By integrating Plaid, Flexport gained access to user-permissioned bank account balances and transaction histories, allowing them to better address client financing requirements and drive growth.

With Plaid's real-time financial monitoring, Flexport no longer relies on monthly financial updates or bank statements, instead gaining immediate insights into their clients' financial health. This access to real-time bank data enables Flexport to minimize risk and offer loans that they might have otherwise deemed too risky. Additionally, Plaid simplifies ongoing reporting for Flexport Capital's clients, reducing their effort and streamlining processes.

Virtual accounts

Virtual account APIs create dedicated account identifiers under a master banking relationship. The pattern is useful when a platform needs reliable reconciliation, client fund segregation, marketplace payouts, wallet-like ledgers, or customer-specific inbound payment references.

The implementation challenge is usually ledger integrity. Product teams should align virtual account APIs with double-entry accounting, payment state machines, treasury reporting, ACH or SEPA settlement windows, and controls for failed, duplicated, or reversed transactions.

Ideal for: Companies with complex payment and collection needs, financial service providers, and fintech companies.

Example APIs:

- Sila: Allows US users to set up digital wallets with dedicated account and routing numbers to facilitate ACH transactions, wire transfers, and improve cash flow and reconciliation processes for fintech applications.

- Plaid Virtual Accounts: Lets UK and Europe users manage the entire lifecycle of payments, including creating, fetching, listing virtual accounts, executing transactions, and even refunding payments.

Case study:

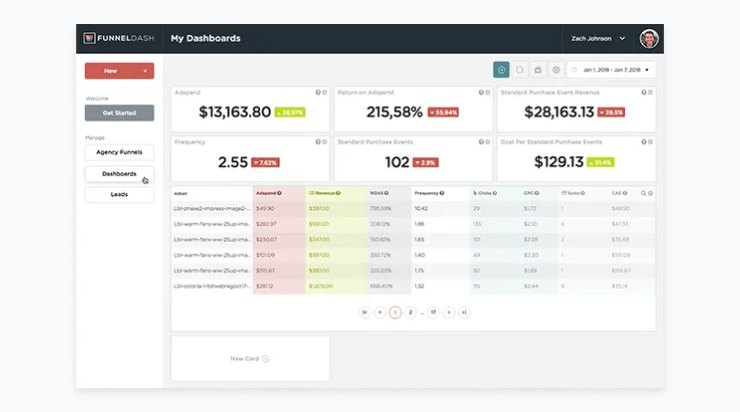

FunnelDash utilized Sila's payment infrastructure and blockchain technology, along with virtual card issuance through a partner, to offer a powerful charge card specifically for digital ad spend. This customized bank card and payment infrastructure is designed to provide cashback and online support tailored for digital ad agencies, which often spend upwards of eight figures annually on advertising.

With Sila's advanced technology, FunnelDash now empowers its users to issue corporate branded virtual and physical cards, enable money transfers and secure bank account linking, send money along the blockchain, and offer solid cashback rewards for card spending. This partnership allows FunnelDash to challenge the status quo and deliver more value to business owners in the advertising industry.

Cryptocurrency APIs

Cryptocurrency APIs provide exchange connectivity, wallet operations, custody workflows, market data, blockchain transaction monitoring, and trading execution. The API layer must handle volatility, latency sensitivity, chain-specific finality, anti-fraud checks, and regulatory reporting obligations.

For B2B fintech products, the main technical risks are custody boundaries, private key management, AML screening for wallet addresses, exchange outage handling, and whether real-time pricing can be trusted for execution, reconciliation, and customer reporting.

Ideal for: Trading platforms, fintech startups, wallet providers, and blockchain developers.

Example APIs:

- CoinGecko API: Provides comprehensive data on cryptocurrency prices, market capitalization, trading volume, and historical data for thousands of digital currencies.

- Coinbase API: Offers access to cryptocurrency trading, wallet management, and real-time price information for various cryptocurrencies available on the Coinbase platform.

- Binance API: Enables trading on the Binance exchange, providing market data, trade execution, and account management features.

- CoinAPI.io: Provides a collection of cryptoAPIs all in one place.

Case study:

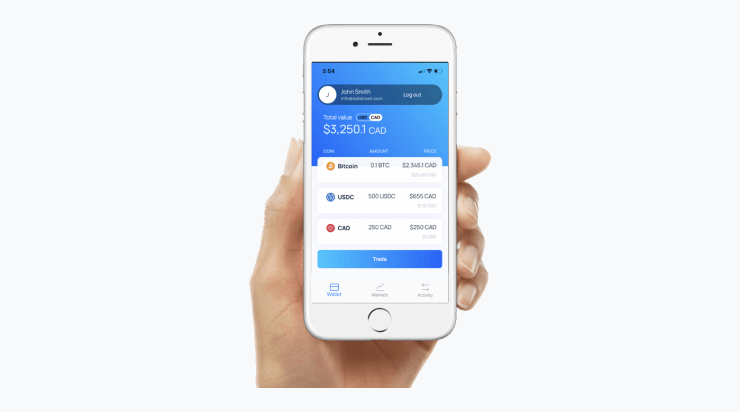

Satstreet needed a reliable real-time cryptocurrency price source to translate complex data into clear insights for their clients and internal use. This capability allows them to efficiently run their trading desk, ensuring superior trade execution services and dependable reporting. Satstreet integrated with CoinAPI's live pricing and charting library.

With CoinAPI, Satstreet ensures their clients have access to essential price data. By aggregating prices from multiple sources, Satstreet provides comprehensive market comparisons, empowering clients to make informed decisions. Satstreet stands out as a premium service provider in the cryptocurrency trading space.

Access market data

Market data APIs provide real-time quotes, delayed prices, historical candles, fundamentals, corporate actions, news, options chains, and reference data from exchanges and data vendors. These APIs support portfolio tracking, automated trading, risk models, investment research, and financial news products.

The architectural questions are specific: whether the API license allows redistribution, which exchanges are covered, how rate limits work during market open, whether websocket feeds are available, and how the platform persists historical data for audits, backtesting, and customer-facing reports.

Ideal for: Financial institutions, trading platforms, investment firms, fintech startups developing trading apps, portfolio management tools, and financial news services.

Example APIs:

- Bloomberg API: Delivers market data, news, and analytics, including comprehensive financial information from global markets.

- Morningstar API: Provides data on stocks, mutual funds, ETFs, and market indices, along with financial metrics and performance analysis.

- Nasdaq Data Link: Offers a variety of datasets including real-time and historical market data, financials, and economic data.

- Polygon.io: Provides access to real-time options prices, historical data, and news on all major options markets including CBOE, NYSE, and NASDAQ.

Case study:

Birdwingo, the first platform of its kind to enter the European market, offers Gen Z and Millennials a way to discover companies and build investment portfolios that align with their personal values and preferences.

Birdwingo quickly became operational thanks to Polygon.io API. By accessing the Starter.feed, they were able to obtain real-time data immediately, allowing developers to create a proof of concept without the need to communicate with any exchanges.

Subsequently, Birdwingo upgraded to the poly.feed product from Polygon.io to display real-time price data from Nasdaq, NYSE, and IEX for their app launch. Additionally, Birdwingo leverages the Ticker Details API endpoint to populate fields such as daily market cap, logos, and standard industry classification codes, creating a rich and engaging user interface for their users.

OCR and machine learning

OCR and machine learning APIs automate document-heavy finance workflows: invoice extraction, bank statement parsing, receipt capture, loan document processing, ID document reading, and compliance evidence collection. Mature OCR APIs combine computer vision, layout analysis, entity extraction, confidence scores, and human-in-the-loop review queues.

In cloud architectures, these workflows often use services such as Google Cloud Vision API, Azure AI Document Intelligence, AWS Textract, Python post-processing pipelines, and queue-based orchestration. Before production rollout, teams should test extraction quality on low-resolution scans, multi-page PDFs, handwritten fields, multilingual documents, and regulated retention requirements.

Ideal for: Financial institutions, fintech startups, insurance companies, and businesses dealing with large data volumes and documents.

Example APIs:

- Google Cloud Vision API: Offers powerful image analysis capabilities, including text extraction from documents, enhancing accuracy and efficiency.

- Azure AI Document Intelligence: Extracts information from forms and documents, automating data entry and processing.

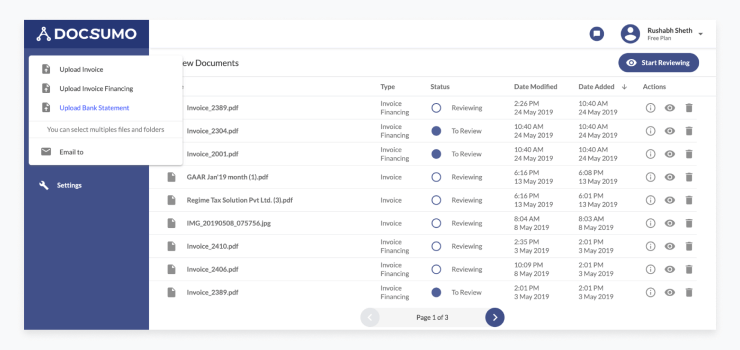

- Docsumo API: Uses OCR technology to convert unstructured documents into actionable information; can work with many types of documents in different formats, including scanned images and PDF files.

Read More: 10 Best AI-Powered OCR Tools for Accurate Data Extraction

Case Study:

As a white-label ATM provider, Hitachi faced significant challenges with monthly reconciliation of bank statements sent by ATM operators. Manual processing proved insufficient due to the increasing volume. By leveraging the Docsumo API, the company was able to process bank statements in less than 30 minutes with an accuracy rate exceeding 99%. The automation of the entire process significantly improved efficiency and accuracy.

What risks do FinTech APIs pose for the financial industry?

Fintech APIs move regulated functions outside the internal codebase, but they do not remove operational accountability. The product owner still needs controls for data security, compliance evidence, incident response, availability, vendor lock-in, and degraded provider behavior.

Security vulnerabilities

Security is the highest-impact risk. Poorly secured fintech APIs can expose PII, transaction data, account tokens, payment credentials, or identity documents. Engineering teams should require OAuth 2.0 or equivalent authorization, least-privilege scopes, signed webhooks, encryption in transit and at rest, key rotation, audit logs, and anomaly monitoring.

Compliance and regulatory challenges

Fintech API usage must align with GDPR, PSD2, AML, KYC, PCI DSS, local banking rules, and the product's own risk policy. Non-compliance can create fines, onboarding delays, bank partner objections, and customer trust issues. Multi-country products also need jurisdiction-specific consent, data residency, and retention rules.

Integration complexity

Multiple providers introduce inconsistent data models, webhook semantics, authentication flows, sandbox fidelity, error codes, and rate limits. Poor integration design can cause duplicated payments, missing reconciliation events, stale bank data, and customer support escalation. Work with an experienced API development team when API behavior affects money movement or regulated decisions.

Dependency on third-party providers

Third-party APIs create vendor dependency. Outages, pricing changes, discontinued endpoints, regional coverage changes, or altered terms of service can affect core product flows. CTOs should define abstraction layers, fallback providers where practical, data export rights, SLA clauses, and migration paths for high-risk integrations.

Performance and scalability issues

Fintech APIs must handle spikes around payroll dates, market open, month-end reconciliation, checkout campaigns, and batch document processing. Performance testing should include provider rate limits, retry storms, idempotency behavior, timeout policies, queue backpressure, and observability in tools such as AWS CloudWatch, Datadog, OpenTelemetry, or equivalent monitoring stacks.

Conclusion

Fintech APIs are the practical route to faster product delivery in regulated finance, but only when API selection includes architecture, compliance, operational resilience, and vendor risk. Payment APIs, KYC APIs, open banking APIs, virtual account APIs, crypto APIs, market data APIs, and OCR APIs can each shorten build time, but each one also moves critical product behavior into a third-party dependency.

SoftKraft provides financial software development services and API development services for teams that need reliable fintech integrations, Python backend engineering, AWS-ready architecture, secure data flows, and compliance-aware delivery. A good discovery phase should identify which capabilities to buy through APIs, which workflows require custom logic, and where the product needs auditability from day one.

![10 Dos and Don'ts - Financial App Development [2025 Guide]](/uploads/blog/financial-app-development/financial-app-development.png)